The future of SEPA access: what it means when the door closes

Across Europe, the payments landscape is shifting. By the end of 2025, some providers will lose their direct connection to SEPA. That means corporates who rely on them for smooth euro payments will feel the effects in cost, in speed, and in certainty.

We think it is important to explain what this change really means. Because behind every acronym, there are businesses trying to pay suppliers, employees waiting for salaries, and treasurers trying to balance liquidity. When direct access disappears, those jobs get harder.

What changes, in numbers

In 2024, CENTROlink, the Bank of Lithuania’s SEPA gateway, processed 294 million payments. Nearly 176 million of those were instant. A huge leap from just 17 million instant payments in 2020. That growth shows how important SEPA Instant has become for European businesses.

But UK licensed EMIs and PIs, who today connect via CENTROlink as “addressable BIC holders,” will lose that connection by 31 December 2025. After that, their agreements end. Only EU or EEA licensed institutions with safeguarding accounts in EU institutions can continue.

It sounds technical. But here is what it really means.

How corporates will feel it

Higher costs. More intermediaries in the chain, each taking a cut.

Slower transfers. Without SEPA and SEPA Instant, funds do not move in real time.

Added complexity. Reconciliation across multiple providers, more room for error.

Liquidity pressure. With new safeguarding rules, the flow of funds tightens.

For a CFO, that means less predictability in cash flow. For a payroll manager, delays in salaries. For a marketplace platform, unhappy customers waiting for refunds. It is friction where there should be flow

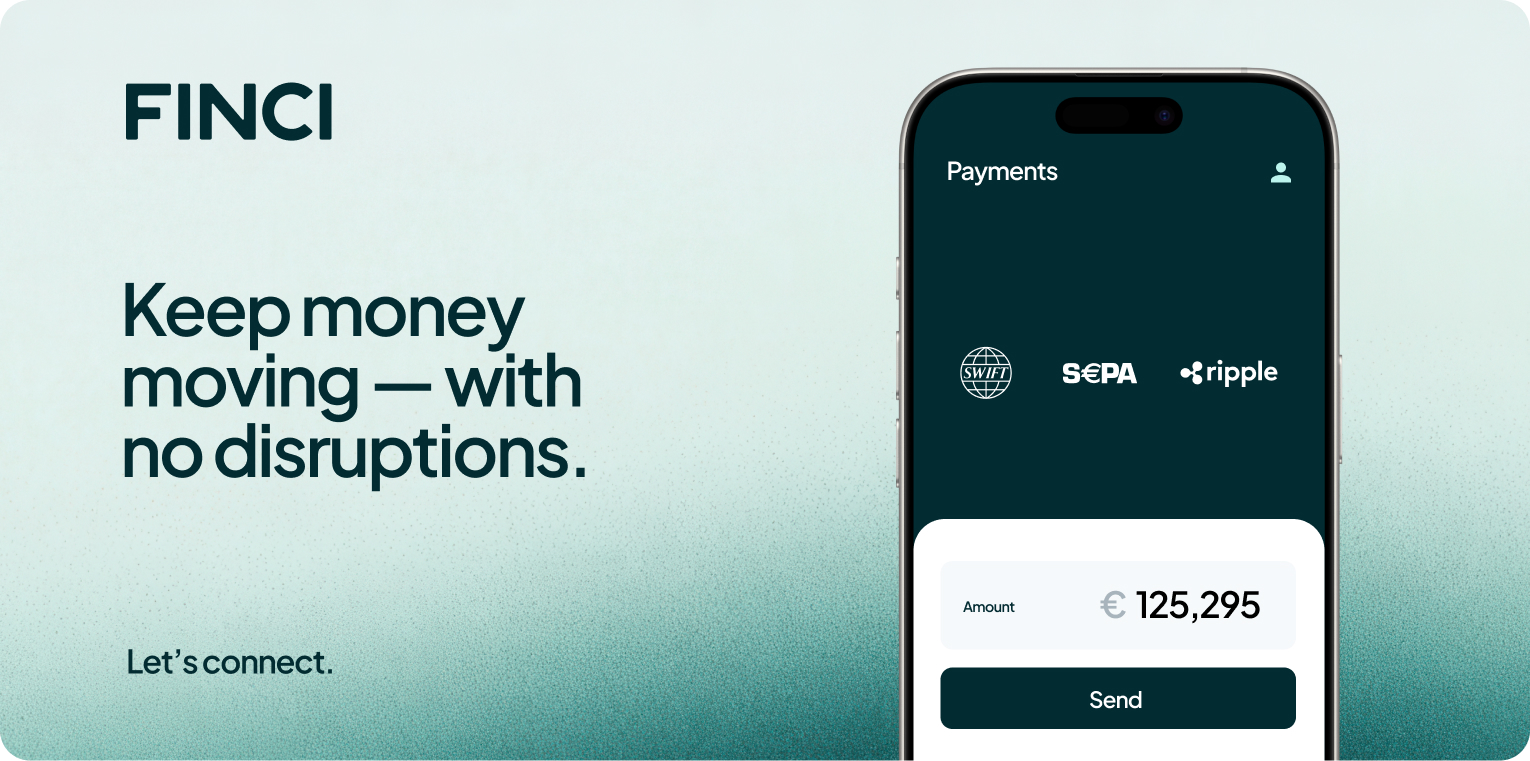

How FINCI helps

At FINCI, our focus is to keep payments moving without disruption. We are licensed in the EU, with direct access to SEPA and SEPA Instant. We complement this with global networks like SWIFT and Ripple, enabling corporates to handle multi-currency payments with greater speed and efficiency.

We have already adapted to the new safeguarding rules, so our clients face no uncertainty as deadlines approach. What they experience instead is continuity: euro payments that remain instant, affordable, and reliable.

Conclusion

The withdrawal of direct SEPA access for some providers is not a mere regulatory detail. It is a catalyst forcing corporates to reimagine their payments infrastructure. Rising costs, slower settlements, and operational risks are real challenges, but also opportunities to partner with providers ready for the future.

At FINCI, we are ready to collaborate with organizations seeking to keep euro payments efficient and inexpensive, maintain instant settlement capabilities, and navigate new regulatory terrain with confidence. Let us start a conversation and explore how your business can emerge stronger from this shift.